The battle lines are drawn, and they run straight through the American housing market.

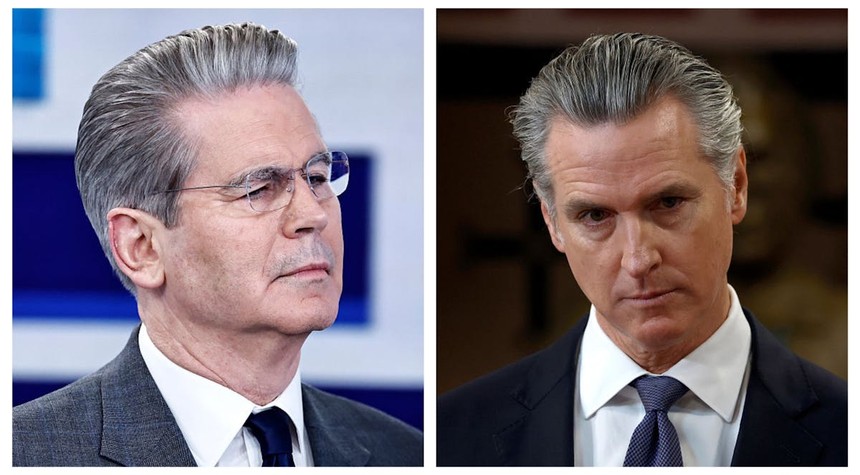

Treasury Secretary Scott Bessent found himself in the crosshairs of California Governor Gavin Newsom this week after laying out the Trump administration’s vision for tackling the housing crisis. The dispute centers on a plan that, frankly, should have been implemented years ago: limiting large institutional investors from gobbling up single-family homes while ordinary Americans struggle to find affordable housing.

Speaking from the World Economic Forum in Davos, Bessent outlined a straightforward approach to distinguishing between the small-time investor and the corporate behemoths that have turned the American dream of homeownership into a bidding war that working families cannot win.

The policy under consideration would restrict large institutional players such as private equity firms and corporate landlords from purchasing single-family homes. These entities have been systematically buying up properties across the nation, reducing available inventory and driving prices beyond the reach of first-time buyers and young families.

Bessent’s explanation was clear and measured. The administration recognizes the difference between parents who invested in a handful of rental properties for their retirement and massive corporate entities deploying billions of dollars to corner local housing markets. The guidance, when issued, will protect the former while reining in the latter.

“We’re going to give guidance, at some point, to see, what is a mom and pop,” Bessent explained. “Someone, maybe your parents for their retirement have bought 5, 10, 12 homes. So we don’t want to push the moms and pops out; we just want to push everyone else out.”

That seems reasonable enough. Yet Newsom, whose state faces perhaps the most severe housing crisis in the nation, took to social media to attack the Treasury Secretary as “smug” and “out of touch.”

The irony here is thick enough to cut with a knife. California, under Newsom’s leadership, has become a cautionary tale of housing unaffordability. The state’s median home price hovers around $800,000, pricing out teachers, nurses, police officers, and countless other working professionals. Meanwhile, institutional investors have been particularly aggressive in California markets, snapping up properties and converting potential homeowners into permanent renters.

Bessent’s response to Newsom’s attack demonstrated the kind of backbone that has been sorely missing from economic policy discussions. Rather than backing down, the Treasury Secretary stood firm on the administration’s commitment to addressing a problem that affects millions of American families.

The truth is that this policy represents a long-overdue reckoning with a housing market that has been distorted by Wall Street’s insatiable appetite for residential real estate. When massive investment firms can outbid individual buyers with cash offers and waived contingencies, the market ceases to function as it should.

The question facing policymakers is not whether to act, but how quickly and decisively they can move to restore balance. The Trump administration appears ready to draw that line in the sand, protecting small investors while pushing back against corporate consolidation of the housing market.

Newsom’s criticism rings hollow when measured against his own record. Perhaps instead of launching attacks from social media, the California governor might consider why his state has become a poster child for housing dysfunction and what his administration has done to address it.

The American people deserve a housing market that works for them, not one optimized for institutional investors’ quarterly earnings reports. Secretary Bessent seems to understand that fundamental truth, even if it makes some politicians uncomfortable.

Related: New Bill Would Strip Citizenship From Naturalized Americans Who Commit Fraud or Felonies